Austin and the surrounding communities — Georgetown, Round Rock, Cedar Park, Leander, Hutto, Pflugerville — are booming. Population growth, a strong job market, and a thriving startup culture make this one of the best places in the country to start and grow a business. At the same time, rising home prices, high property taxes, and a competitive labor market create real financial pressure for local entrepreneurs.

Add in Texas’ unique features — no state income tax, a relatively business-friendly tax structure, strong homestead protections — and you get a landscape where smart, integrated financial planning isn’t a luxury. It’s the difference between building durable wealth and constantly fighting fires.

As your financial partners at Axon Capital Management, we recognize that mastering these challenges is the first step toward long-term wealth creation.

This condensed checklist walks through the core areas Austin-area business owners should pay attention to: business structure, cash flow, taxes, retirement, risk management, growth, personal finances, and exit planning.

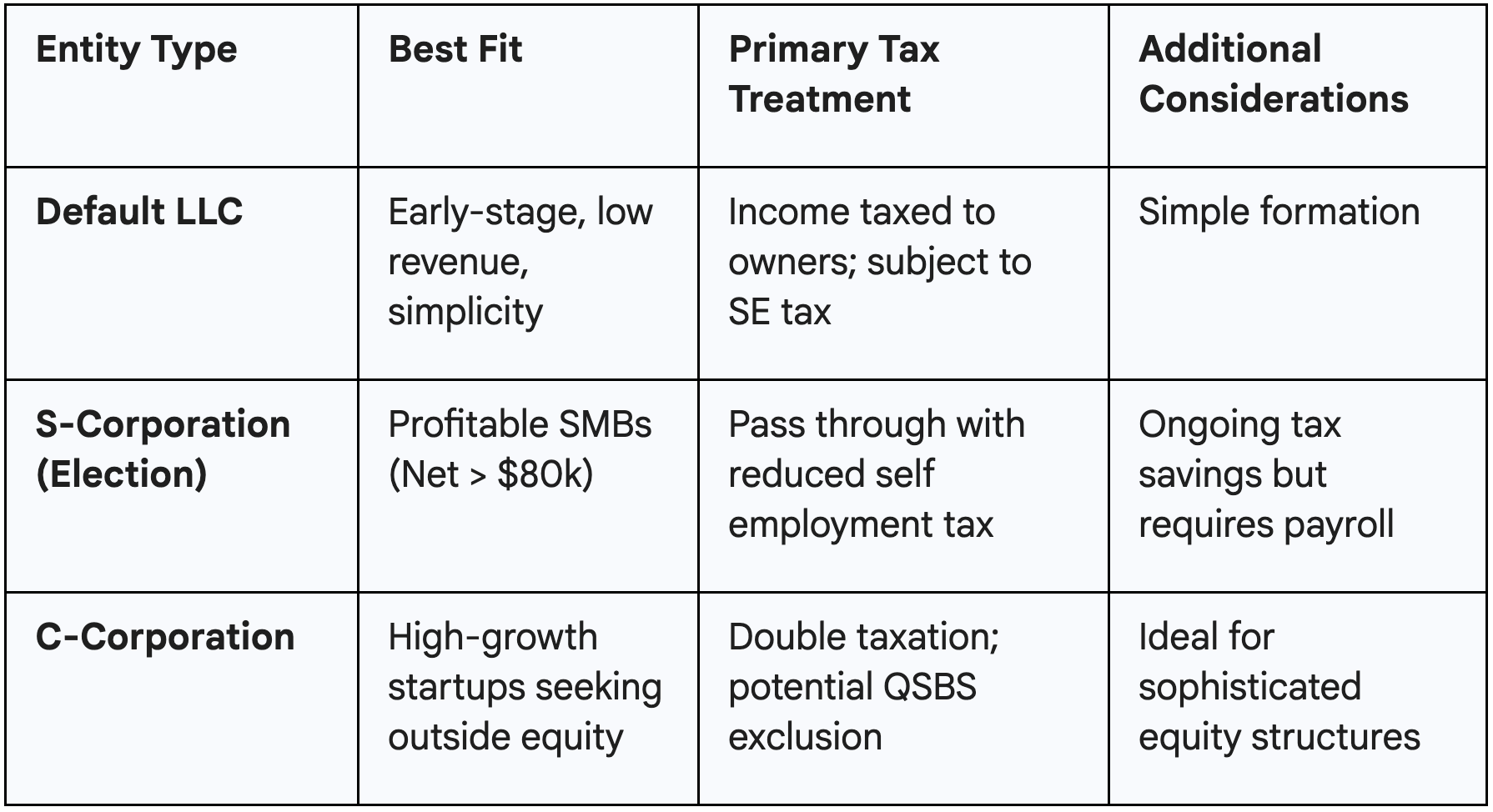

The structure you choose for your business will influence your taxes, liability exposure, administrative burden, and even how easy it is to sell one day. In Central Texas, many small businesses operate as LLCs taxed as sole proprietorships or partnerships, or as LLCs and corporations that elect S-corporation status. High-growth startups — especially those chasing venture capital — often end up as C-corporations, frequently incorporated in Delaware.

An LLC is a common starting point because it’s flexible, relatively simple to maintain, and provides a liability shield if you respect the separation between you and the business. By default it’s treated as a pass-through entity, meaning profits flow onto your personal return. An S-corporation election, once profits are high enough, can reduce self-employment tax by splitting your compensation between salary (subject to payroll tax) and distributions (generally not). A C-corporation can make sense if you aim for institutional investment and want to issue stock and options broadly, but it introduces corporate tax and more complex compliance.

Whatever structure you choose, the non-negotiable step is to separate business and personal finances from day one. That means obtaining an EIN, opening business bank accounts and credit cards, running revenue and expenses through those accounts, and using basic accounting software. This isn’t just about neat books; it’s central to preserving your liability protection and knowing whether the business is actually profitable. Commingling funds makes tax time harder, invites errors, and can weaken your protection if a creditor or plaintiff tries to argue that you and the business are really the same thing.

Texas’ franchise tax is an additional piece of the puzzle. It is not an income tax, and many smaller businesses fall below the revenue threshold and owe nothing, but you may still have to file a simple report each year. A local CPA can clarify your obligations and help you decide if and when to make an S-corp election or other structural changes.

For many Austin business owners, cash flow is lumpy by nature. A contractor in Leander might experience big checks during busy building seasons and stretches of quiet. A marketing agency in downtown Austin might land one large client that carries several months of revenue, then wait for the next big project to close. Unlike a salaried W-2 employee, you do not have a guaranteed paycheck arriving every two weeks.

The starting point is to know your baseline numbers: what it costs each month to keep the business open, and what it costs to keep your household afloat. On the business side this includes rent or coworking fees, software, payroll, insurance, and debt payments. On the personal side it includes housing, groceries, utilities, insurance, transportation, childcare, and debt. Once you have those figures, you can back into a conservative but realistic owner salary or draw and pay yourself on a regular schedule — even if the business receives income in bursts.

Treating yourself like an employee brings order to what would otherwise be chaos. Instead of raiding the business account whenever there’s extra cash, you transfer a fixed amount each month and let the business retain the surplus as a buffer. In strong periods, that extra cash builds up in a business emergency fund that can cover lean months, temporary closures from storms, or late-paying customers. On the personal side, you also want a robust emergency fund, often six to twelve months of living expenses for self-employed people, given the added uncertainty of owning a business.

A simple but powerful tactic is to create a dedicated tax savings account and automatically move a percentage of every dollar of revenue into it. Federal income taxes, self-employment or payroll taxes, and, if applicable, Texas sales tax can otherwise sneak up on owners who are focused only on net cash in the operating account. By “paying the tax man first” in this way, you minimize the chance of being surprised by a large bill you’re not prepared to pay.

Planning around seasonality and known large outflows is equally important. If you know that most of your revenue arrives in the last quarter of the year, you might avoid locking in large fixed costs in the spring. If annual insurance renewals, software contracts, or property tax payments always land in certain months, those should be built into your cash flow calendar so they don’t feel like emergencies when they arrive.

The overall objective is to transform irregular business cash flow into stable personal income and to ensure both your company and your household can ride out the inevitable ups and downs of the Austin economy. A financial planner can help you build systems, budgets, and safeguards that make that stability possible.

Texas gives entrepreneurs a significant edge by not taxing personal or corporate income. A business owner with pass-through profits or a salary from their own company will not owe state income tax on that money. This is a meaningful difference compared to high-tax states and can free up cash to reinvest in the business or save for the future.

However, the absence of state income tax does not mean the tax picture is simple. Federal income taxes still apply, and if you are a sole proprietor, partner, or owner of an LLC taxed as a partnership, you will likely pay self-employment tax on your share of net earnings. S-corporations and C-corporations introduce payroll tax dynamics that require careful handling: owners must pay themselves reasonable salaries, run payroll consistently, and treat distributions or dividends correctly.

Planning ahead for quarterly estimated federal tax payments is crucial. Work with your CPA to forecast profits, factor in deductions, and calculate appropriate payments for April, June, September, and January. Common deductions for Austin-area businesses include home office expenses for those working from home in suburban communities, local business travel across the metro, equipment purchases, and qualified retirement plan contributions.

In addition to income-related taxes, Austin businesses need to pay attention to sales tax and tangible personal property tax. If you sell taxable goods or certain taxable services, you must collect and remit sales tax at the combined state and local rate. Businesses with significant equipment, furniture, or inventory typically must file an annual rendition so counties can assess business personal property taxes. Many small business owners are surprised by this requirement, so it is worth discussing with your CPA to avoid penalties.

Given how intertwined your business and personal finances are, tax planning should be an ongoing, strategic exercise rather than a once-a-year scramble. A capable financial advisor can help you choose and adjust your entity structure, optimize deductions, design compensation strategies, and integrate retirement savings into your overall plan.

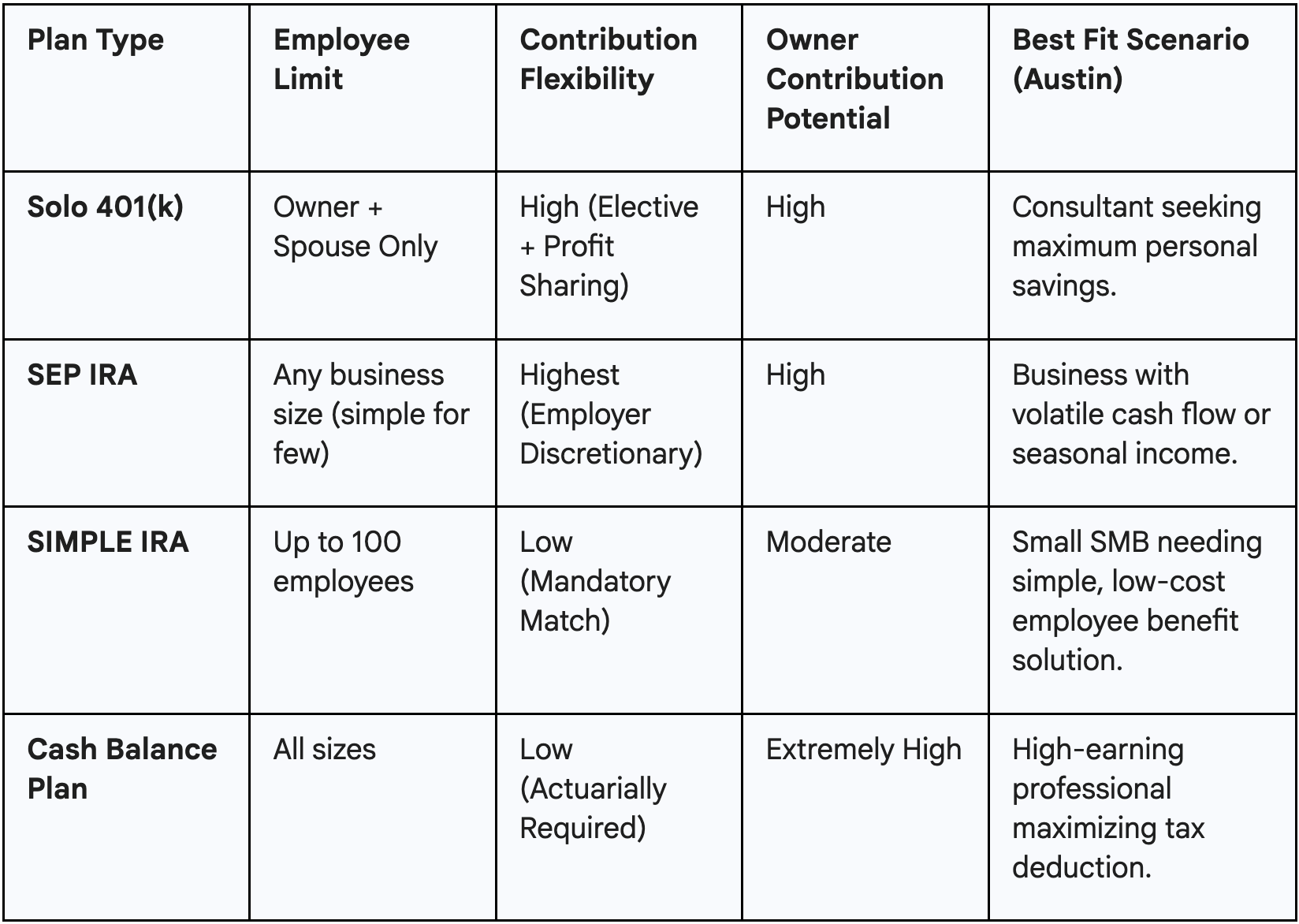

As a business owner, you don’t have a built-in 401(k) with a matching contribution waiting for you. The responsibility to create a retirement plan falls on your shoulders — but that also means you have access to tools that can be more generous than what many employees enjoy.

For solo owners and very small businesses, vehicles like SEP IRAs and Solo 401(k)s are often the first step. A SEP IRA is easy to set up and allows contributions based on a percentage of your net income, up to relatively high dollar limits. It is especially attractive in years when profits are strong, as you can make large contributions close to tax filing time. The tradeoff is that if you have employees, you generally must contribute the same percentage for them as you do for yourself, which can become expensive.

A Solo 401(k) is designed for businesses with no employees other than the owner and possibly a spouse. It lets you contribute in two ways — as the “employee,” via salary deferrals, and as the “employer,” via profit-sharing contributions. This structure allows very high total contribution limits even at moderate income levels and often includes the ability to make Roth contributions or borrow from the plan. It requires a bit more administration, especially as assets grow beyond certain thresholds, but for many solo professionals it is the most powerful and flexible choice.

As your team grows, you may consider a SIMPLE IRA or a traditional 401(k). A SIMPLE IRA offers a straightforward way to give employees the ability to save, with required employer contributions but minimal regulatory complexity. A full 401(k) involves more setup cost and ongoing compliance — including annual nondiscrimination testing — but can be an important part of competing for talent and allows higher contribution limits and plan design flexibility. Recent federal legislation provides tax credits to help small businesses offset some of the costs of starting retirement plans, making them more accessible than many owners assume.

For higher-income owners, particularly in professional practices, adding a cash balance or other defined benefit plan on top of a 401(k) can supercharge retirement savings. These plans require actuarial design and consistent funding but can allow very large pre-tax contributions in the years when owners are earning the most and trying to catch up for later retirement.

Whatever path you choose, the key is not to neglect your own retirement because you are preoccupied with building the business. The ideal is to grow retirement accounts and other investments in parallel with your company so your future does not depend entirely on selling the business at exactly the right time. A retirement planner can help you balance these priorities, ensuring you build personal wealth alongside your business.

Running a business always involves uncertainty. Some risks you consciously take on; others you want to transfer or mitigate. A thoughtful risk management plan covers both the business and the owner.

On the business side, most companies need a mix of general liability, property, and, where relevant, professional liability insurance. Retailers, restaurants, and other brick-and-mortar businesses in the Austin area may be particularly sensitive to slips, falls, or on-premise injuries, while service firms and consultants face risks tied to the quality and impact of their advice or deliverables. Businesses that rely on physical assets — like vehicles, specialized equipment, or leases — need appropriate property and auto coverage. In addition, business interruption coverage can help replace income and cover fixed expenses if a covered event forces you to shut down temporarily, which is not a far-fetched risk in a region that has seen severe storms and infrastructure disruptions.

For small, owner-driven companies, key person insurance is often worth serious consideration. If one founder drives sales, holds crucial technical knowledge, or has relationships that are difficult to replicate, a sudden death or disability could devastate the business. A life or disability policy owned by the business on that person can provide funds to hire replacements, pay down debt, or simply buy time to regroup.

On the personal side, owners should think like their own human resources department. Health insurance, whether obtained through the individual marketplace, a group plan, or a spouse’s employer, protects against catastrophic medical costs. Long-term disability insurance protects your income if an illness or injury prevents you from working.

Beyond pure insurance, Texas law offers powerful asset protection tools when used correctly. The state’s homestead protections can shield a primary residence (within certain acreage limits) from many creditor claims, and retirement accounts often enjoy strong protections as well. Pairing these legal safeguards with the proper use of LLCs and corporations — and with clear contracts, waivers where appropriate, and basic estate planning — can create a robust framework that lets you take calculated business risks without putting your family’s entire balance sheet on the line.

Growth is exciting, especially in a region with as much momentum as Greater Austin. It also changes your financial profile. Adding employees, leasing office space, or expanding to a second location in a suburb like Georgetown or Cedar Park introduces new fixed costs and obligations that must be carefully planned.

The local labor market has been competitive, particularly for skilled roles. Larger employers — from tech giants to healthcare systems — set a high bar for compensation and benefits. Small and midsize businesses that can’t match those numbers dollar-for-dollar often compete through flexibility, culture, growth opportunities, and thoughtful benefits. Offering some form of health insurance, retirement plan, and paid time off can make a disproportionate difference in both recruitment and retention. The cost of these benefits, along with payroll taxes, workers’ compensation if elected, equipment, and training, means the true cost of an employee is materially higher than their base salary. Owners should run numbers using “fully loaded” costs rather than just the headline pay figure.

Office space is another key decision. Austin’s commercial real estate market has shifted with the rise of remote work; vacancies and sublease opportunities mean some businesses can negotiate favorable deals. At the same time, traffic congestion and long commutes make remote or hybrid arrangements attractive to many workers and can reduce overhead if executed thoughtfully. Some owners opt for a small physical footprint — a modest office or coworking membership — combined with remote work policies and periodic in-person gatherings.

As growth accelerates, so does the need for capital. A line of credit to smooth out working capital, term loans for build-outs or equipment, and, in some cases, outside equity investment can all be part of the toolkit. Establishing a relationship with a bank early, maintaining clean financial records, and regularly reviewing key metrics like gross margin, operating margin, and cash conversion cycles will help you grow without outpacing your financial infrastructure.

Your business is a major asset, but it is not the entire story. Personal financial planning is especially important for entrepreneurs because your income is tied to a venture that inherently carries more uncertainty than a typical job.

Structuring your household budget around a conservative, steady salary from the business — rather than treating every strong month as the new normal — is a crucial starting point. If you increase lifestyle spending every time profits spike, you will have a hard time dialing it back when the next downturn arrives. Anchoring your lifestyle to a level you can sustain in average or slightly below-average years, and using surplus cash to build savings, pay down debt, or invest, creates resilience.

In Austin and its suburbs, high housing costs and property taxes demand special attention. A home purchase that stretches your budget too far can turn into a strain when business slows, especially if you also face rising insurance premiums and utility costs in a hot climate. It may be prudent to be more conservative with personal debt — mortgages, car loans, credit cards — than a comparable W-2 earner would be, simply because your income is more variable.

Diversification is another core principle. It might feel natural to reinvest every dollar back into the business, especially in the early years. Over time, though, building a portfolio of retirement accounts, taxable investments, and perhaps other assets like real estate creates additional pillars of wealth that are not all tied to the same risk. If something happens to your company or your industry, your entire net worth is not at the mercy of a single outcome.

Estate planning deserves a mention as well, particularly in a community property state. Having a will, basic incapacity documents, and, where appropriate, trusts or buy-sell agreements ensures there is a plan for your business and your assets if something happens to you. This is not just about taxes; it is about avoiding confusion, conflict, and forced decisions during already difficult times.

Every business will have an ending: sale, succession, or wind-down. Thinking about that future — even in broad strokes — can meaningfully shape the decisions you make today.

If you imagine eventually selling to a third party, it pays to build your company with that future buyer in mind. Clean, transparent financial statements, documented processes, a management team or at least staff who can handle operations without you, and a diversified customer base all make a business more attractive and valuable. If your plan is to pass the company to children, partners, or key employees, having a clear succession plan, cross-training, and appropriate legal agreements in place avoids confusion and disputes later.

Texas offers some structural advantages in exit planning. There is no state income tax, so proceeds from selling your business interest are not subject to state capital gains tax. There is also no state estate or inheritance tax, though federal rules may still affect larger estates. Within that framework, strategies involving trusts, gradual gifting, or family entities can help you transition ownership over time while managing federal taxes and maintaining control.

From a personal financial planning perspective, it is essential to connect your exit assumptions to your long-term goals. If you are counting on selling the business at a certain age for a certain amount, it is worth modeling what that would need to look like after taxes and fees and comparing it to your desired retirement lifestyle. If the numbers do not match, you can adjust in several ways: changing timelines, revising spending expectations, increasing saving and investing outside the business, or focusing more intentionally on boosting the company’s value.

Owners who prepare for an exit early — even in small ways, like cleaning up books, clarifying roles, and gradually stepping out of day-to-day operations — tend to have more options and better outcomes than those who wait until they are exhausted or facing external pressure.

Being a business owner in the Austin area is both an opportunity and a responsibility. The opportunity lies in a dynamic, growing economy with no state income tax and a culture that celebrates entrepreneurship. The responsibility lies in the fact that nobody is doing your financial planning for you. You must design a structure that supports both the business and your household, manage cash flow deliberately, navigate taxes, protect against risks, save for retirement, and think ahead about eventual exits.

You do not have to tackle everything at once. Choose one or two areas that feel most urgent — perhaps separating business and personal finances more clearly, building up an emergency fund, or finally establishing a retirement plan — and make concrete progress there. Then, as your business evolves, revisit the other pieces: entity structure, insurance, growth strategy, personal investing, and exit planning.

Above all, remember that your business and your personal finances are two sides of the same coin. A stronger business foundation makes your personal life more secure, and a healthier personal balance sheet makes you a more resilient, clear-headed owner. With intentional planning — and with the support of a fiduciary advisor like Axon Capital Management — you can enjoy the rewards of building a company in Central Texas while also creating long-term financial stability for yourself and your family.

Article written by Brady Lochte, founder of Axon Capital Management and a fee-only fiduciary financial advisor serving individuals and families across the Austin metro area. Brady is committed to providing clear, transparent financial guidance that helps people navigate retirement, investing, and long-term planning with confidence.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, legal, or tax advice. Readers should consult with their own financial, legal, and tax professionals before making any decisions based on the content of this article. Past performance is not indicative of future results. All examples and strategies discussed are illustrative and may not be suitable for all individuals.

Please submit the form with any questions or comments and I'll be in touch shortly.

If you'd rather not wait, you can also book a time directly on my calendar using the link below:

Schedule a call