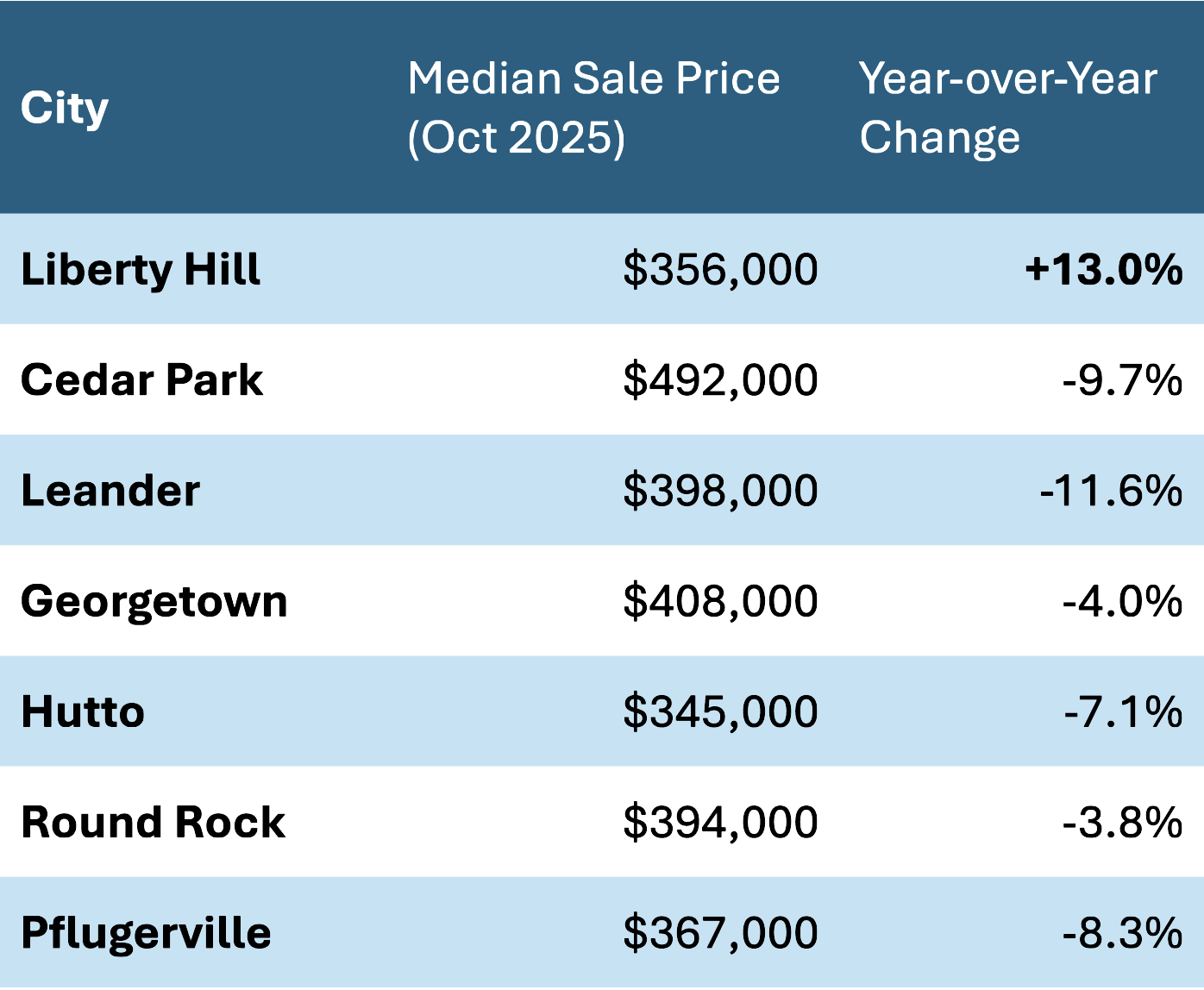

Understanding the local real estate market is critical for effective financial planning, especially when deciding where to buy a home. In the Austin metro area, suburban cities like Liberty Hill, Cedar Park, Leander, Georgetown, Hutto, Round Rock, and Pflugerville each offer different price points. Below we compare the median prices of single-family homes in these areas as of late 2025.

Liberty Hill — With a median single-family home price of about $356,000 (up 13% year-over-year), Liberty Hill is showing strong price momentum. The relatively lower entry cost combined with significant appreciation signals that buyers may be capturing value earlier in the growth cycle. For financial planning, that means lower upfront housing cost, but potentially higher future market risk if growth expectations accelerate.

Cedar Park — The median sale price stands around $492,000, having fallen roughly 9.7% from the prior year. Although higher priced than many suburbs, Cedar Park’s proximity to Austin and mature infrastructure give it resilience.

Leander — Median home prices are near $398,000, with a year-over-year decline of about 11.6%. Leander’s drop suggests an affordability adjustment is underway. For clients, it means opportunity but also caution: lower cost may stretch budgets less, but slower appreciation could impact long-term wealth accumulation.

Georgetown — Median single-family prices are approximately $408,000, with slight year-over-year decline (around 4%) in recent data. Georgetown offers a middle ground: moderate price, established community, and steady—but not explosive—growth.

Hutto — Homes in Hutto have a median price around $345,000, one of the more affordable options among the suburbs. While growth may be more modest, the lower entry cost can free up capital elsewhere in the plan (such as investing or retirement savings).

Round Rock — With median home values around $394,000, Round Rock remains competitively priced relative to its amenities, schools, and growth profile. For families prioritizing stability, Round Rock offers a good balance of price and quality. In a financial-planning context, it may allow a higher down payment or shorter mortgage term while still accessing strong community features.

Pflugerville — Median single-family prices hover near $367,000, offering a compelling blend of affordability and access to the Austin metro. From a planning perspective, Pflugerville may enable homeownership earlier or with lower budget stress, which can help clients preserve liquidity for other goals (education, retirement, emergency savings).

From a homebuyer’s perspective, this means the typical budget required for a house varies significantly by location. A family shopping in Cedar Park or Georgetown should expect to spend around $400K–$500K for a median-priced home, whereas in Hutto, Liberty Hill, or Pflugerville, the mid-$300Ks might suffice for a comparable property.

These medians are just benchmarks – individual listing prices will range above and below – but they give a sense of relative affordability. For instance, one might save $100K+ by choosing a home in Hutto or Liberty Hill versus a similar home in Cedar Park. Of course, price is only one element of affordability; we must also weigh ongoing costs like Williamson County property taxes.

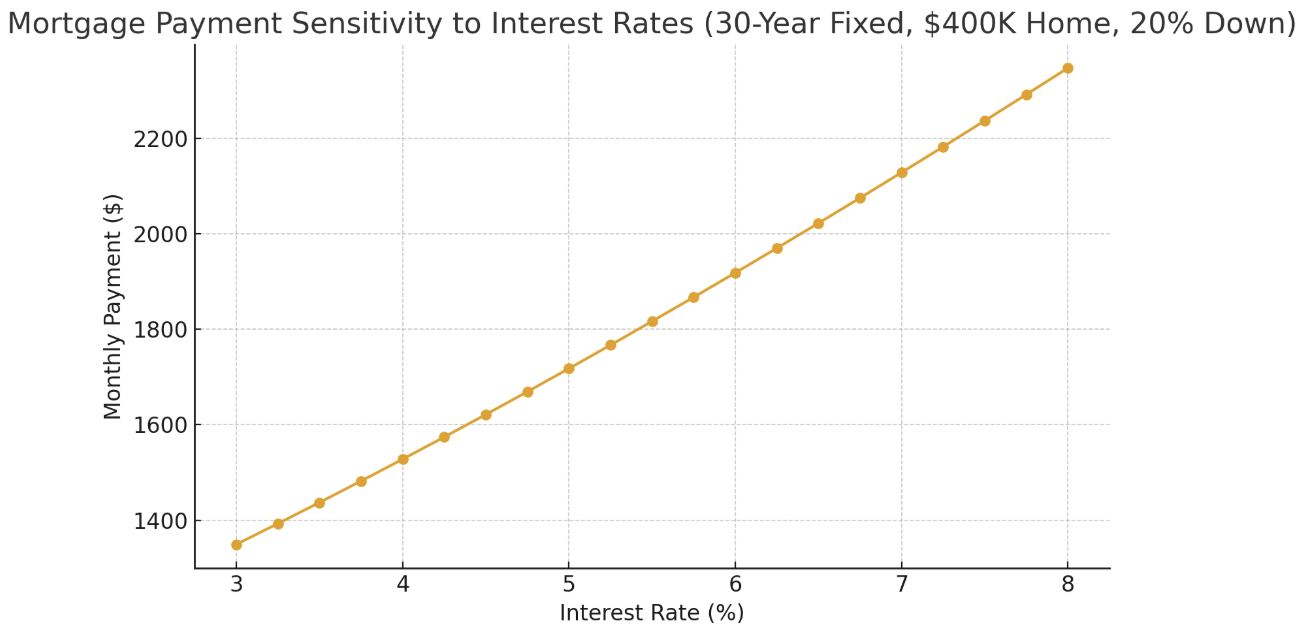

Interest rates can have just as much impact on affordability as home prices themselves. In fact, a 1% change in the mortgage rate can shift a family’s monthly payment by hundreds of dollars — often enough to change which suburb or price point fits comfortably within budget.

For example, consider a 30-year fixed mortgage on a $400,000 home with 10% down. At a 6.0% interest rate, the principal and interest payment is roughly $2,158 per month. If rates rise to 7.0%, that same home now costs about $2,395 per month — an extra $2,800 per year in interest expense. Conversely, if rates drop to 5.0%, the payment falls to around $1,930 per month, freeing up nearly $225 per month of cash flow.

These differences matter when comparing areas like Cedar Park vs. Liberty Hill or Round Rock vs. Hutto. A buyer in Cedar Park might pay $100K more for a similar home, but if they lock in a lower interest rate or buy during a rate dip, their monthly payment could be similar to someone buying a cheaper home at a higher rate. This dynamic underscores why timing and financing strategy are as important as location in the Austin market.

At Axon Capital Management, we help clients model these scenarios before they commit to a home purchase. We test “what-if” cases for different loan types, down payments, and interest rates, showing exactly how a change in borrowing costs affects the total financial plan. We also coordinate when rate buydowns, adjustable-rate loans, or larger down payments make sense given broader investment goals.

By integrating home financing into their overall financial plan, families can make better-informed decisions — not just about which home to buy, but when and how to buy it.

For many in the Austin metro area — especially young professionals and relocating families — the question isn’t just where to live, but whether to buy at all. With home prices moderating but mortgage rates still elevated, the rent-versus-buy equation has become more nuanced.

As of late 2025, average rents for a three-bedroom home range from about $2,100–$2,400 in Round Rock and Pflugerville, and closer to $2,600–$2,800 in Cedar Park or Leander, depending on neighborhood and amenities. Meanwhile, a median-priced home in those same areas might carry a total monthly payment (including mortgage, insurance, and taxes) between $2,600 and $3,000. In other words, buying often costs a few hundred dollars more per month up front — but it begins building equity immediately.

From a financial planning perspective, the decision hinges on three factors:

Renting can make sense for mobility or short-term affordability; buying can make sense for long-term wealth-building and stability. What matters most is understanding the trade-offs in the context of your broader financial picture — cash flow, investment strategy, and career outlook.

At Axon Capital Management, we use data-driven analysis to help clients answer this question with confidence. Whether you’re deciding between renting in Austin or buying in Georgetown, or weighing a move to a growing area like Liberty Hill, we model both options side by side so you can see which path best supports your long-term plan.

Choosing a home is not just a real estate decision – it’s a financial planning decision. The comparison of home prices in Liberty Hill, Cedar Park, Leander, Georgetown, Hutto, Round Rock, and Pflugerville highlights how holistic planning is necessary to make the best choice:

Bottom line: Real estate decisions should be made with both head and heart – considering numbers and lifestyle. By comparing median home prices across Austin’s suburbs, we see tangible differences that will affect a family’s finances for years to come. Taxes and school quality further shape the equation of what’s “affordable” or “worth it” for you. This is where a fiduciary financial advisor can provide value. Our role is to help you make an informed decision about homeownership within the bigger picture of your financial life.

Homeownership can be a powerful step in building long-term wealth, and with careful planning, you can enjoy that new home without derailing your other goals. We’re here to help you map out that path, so you feel confident that your home purchase is not just a dream come true, but also a sound investment in your future.

If you have questions about buying a home, comparing mortgage options, or how housing fits into your broader financial plan, fill out the form below. We’ll schedule a brief, no-obligation consultation to help you make confident, well-informed decisions.

Article written by Brady Lochte, founder of Axon Capital Management and a fee-only fiduciary financial advisor serving individuals and families across the Austin metro area. Brady is committed to providing clear, transparent financial guidance that helps people navigate retirement, investing, and long-term planning with confidence.

Disclaimer: This article is provided for informational and educational purposes only and should not be construed as personalized financial or investment advice. The examples and figures presented (including home prices, mortgage rates, and cost estimates) are based on publicly available data as of late 2025 and are subject to change. Past market trends do not guarantee future results. Before making any financial or real estate decisions, you should consider consulting a qualified professional who can provide guidance based on your individual circumstances.

Please submit the form with any questions or comments and I'll be in touch shortly.

If you'd rather not wait, you can also book a time directly on my calendar using the link below:

Schedule a call