Name, Image, and Likeness (NIL) deals have opened new financial doors for college athletes, creating opportunities to earn significant income while still in school. But with great opportunity comes great responsibility. This guide will show how top college athletes – and their families – can turn short-term NIL income into long-term financial stability. We’ll cover why this windfall is unique, how easy it is to squander, and the essential money principles and strategies that can help ensure today’s earnings become tomorrow’s security. The tone here is clear, encouraging, and aimed at both athletes and parents. Let’s dive into the playbook for lasting wealth.

Disclosure: Axon Capital Management is a fiduciary financial advisory firm. The information provided in this guide is for educational purposes only and is not intended as personalized financial advice.

In the past, student-athletes were forbidden from profiting off their sports. That changed in 2021 when the NCAA began allowing athletes to earn money from their Name, Image, and Likeness (NIL)—compensation for the commercial use of their personal brand and identity through endorsements, social media partnerships, and other deals.

NIL has quickly become a billion-dollar market, with top college athletes signing agreements worth $4–5 million. For many, this is the first chance to earn "pro-level" money before turning professional, creating some of the youngest self-made millionaires in the country. NIL income can fund better training, support families, or provide financial comfort most college students never experience.

With proper planning, NIL earnings represent a game-changing opportunity for athletes to leverage their talent into real money—and potentially the foundation for multi-generational wealth.

Despite the huge opportunity, there’s a very real danger: most athletes risk squandering their NIL earnings if they’re not careful. Being young and suddenly well-paid can lead to costly mistakes. Many of these newly wealthy college athletes are among the least prepared to manage their newfound riches. It’s easy to see why – juggling classes, games, and endorsement deals is a tall order for any young person, especially if they come from a background with little financial education. Without guidance, impulsive spending, poor planning, or even scams and bad advice can drain away the money as quickly as it came.

History provides cautionary tales. Professional athletes famously struggle with money after their careers end. A widely cited report found that around 78% of NFL players faced financial stress or bankruptcy within just two years of retirement, and about 60% of NBA players went broke within five years. The exact numbers can be debated, but the message is clear: a high income in your 20s doesn’t guarantee lasting wealth. The real tragedy is that many athletes who earned millions end up with little to show for it, not because they never had money – but because they failed to invest and build wealth with it. They might spend it all on luxury cars, big houses, or help to every friend and relative, only to find themselves struggling financially a few years later.

For college athletes, the risk is even sharper. Most won’t sign pro contracts after college. That means your NIL earnings could be the largest athletic paycheck you ever get. It might have to last you a long time. If it’s blown on short-term splurges, you may miss the chance to secure your future. Overspending, neglecting taxes, or failing to plan for life after college can quickly consume the benefits of NIL deals. The good news? With some smart moves, you can avoid these pitfalls. Below, we outline key financial principles and strategies to ensure you don’t “fumble the bag” but instead score a financial touchdown for your future.

An athletic career – especially at the college level – is often a short window for earning money. Whether or not you go pro, your peak sports income might be confined to a few years in your late teens and early 20s. By comparison, life after sports is long. Professional leagues have average career lengths of just 3–5 years, and many college stars won’t play pro at all. In other words, you could be making good money now, but you might need to rely on those earnings (and whatever they grow into) for decades to come.

Always remember: today’s NIL paycheck might be temporary, but your life after sports is long. Treat this income as if it may have to feed, house, and support you long after the cheering stops. It’s tempting to live large in the moment – buying the fanciest car or treating all your friends – but think beyond today. Discipline now means freedom later. Young athletes often want to buy the car or buy the house for their family, and it’s a wonderful goal – but it must be done in moderation so it doesn’t leave you in a financial hole.

The mindset to adopt is this: Use your short earning window to set up a long, comfortable life. A few years of high income, if managed wisely, can potentially fund many years of stability. In fact, even if you only had, say, three years of strong NIL earnings, invested properly those could put you on a path to early financial independence. So, keep your eyes on the long game. Every dollar you save and invest now is a dollar working for Future You.

The first step to lasting financial stability is creating a budget – essentially, a game plan for every dollar you earn. A budget ensures that you control your money, rather than it controlling you. Start by figuring out your key categories: needs, wants, savings (and investments). For each NIL check you receive, decide how much goes to necessities (like rent, groceries, basic living costs), how much (if any) can go to “fun” or discretionary purchases, and how much you will pay yourself first by putting into savings and investments. By allocating a portion to each category, you make sure you cover today’s needs while still planning for tomorrow.

Budgeting isn’t about saying “no” to everything fun – it’s about making sure you can say “yes” to the important things now and later. If you have a clear plan (maybe with the help of your parents or a trusted advisor), you’ll know how much is safe to spend on a new phone or a celebratory dinner, without derailing your future. Smarter spending choices today – like not going wild on flashy cars or clothes – frees up more money to put toward a house down payment or other big goals tomorrow. Remember, as an athlete you already understand discipline; managing money is just another field to apply that discipline. A solid budget is like a good playbook – it guides your actions and increases your chances of success.

Live below your means, even if your means have grown. It’s easy to feel rich when big checks start coming in, but remember that income can fluctuate or end abruptly. Avoid the trap of “lifestyle inflation,” where higher income leads to higher spending on luxuries. Many pro athletes have fallen victim to this – buying multiple cars, designer clothes, and expensive vacations – only to find out too late that they overspent. You don’t have to live like a monk, but do keep your spending in check. For example, maybe limit big splurges to a small fraction of your NIL earnings and make them one-time treats, not ongoing expenses.

One technique is to use separate accounts for different purposes. Consider keeping your NIL money in a dedicated checking account, and then set up a separate savings account where you automatically transfer a chunk (say, 30% or more) of each payment as soon as it comes in. This way, you’re paying yourself (your future self) first, and you won’t be tempted to spend everything in your primary account. Some athletes even divide their budget into buckets like: 50% needs, 30% savings/investments, 20% wants – or whatever mix fits their goals. The exact percentages can vary, but the principle stands: budgeting helps you prioritize and ensures you don’t accidentally burn through your money.

Saving is the flip side of budgeting: once you spend less than you earn, you’ll accumulate savings that need a purpose. The smartest purpose for long-term savings is investing – putting money to work so it grows over time. For young athletes, investing early is a powerful move. Why? Because of the miracle that is compound interest. In simple terms, compounding means your money can earn money (through interest or investment returns), and then that new money also earns money, and so on – like a snowball rolling downhill. The more time you give it, the bigger it can grow.

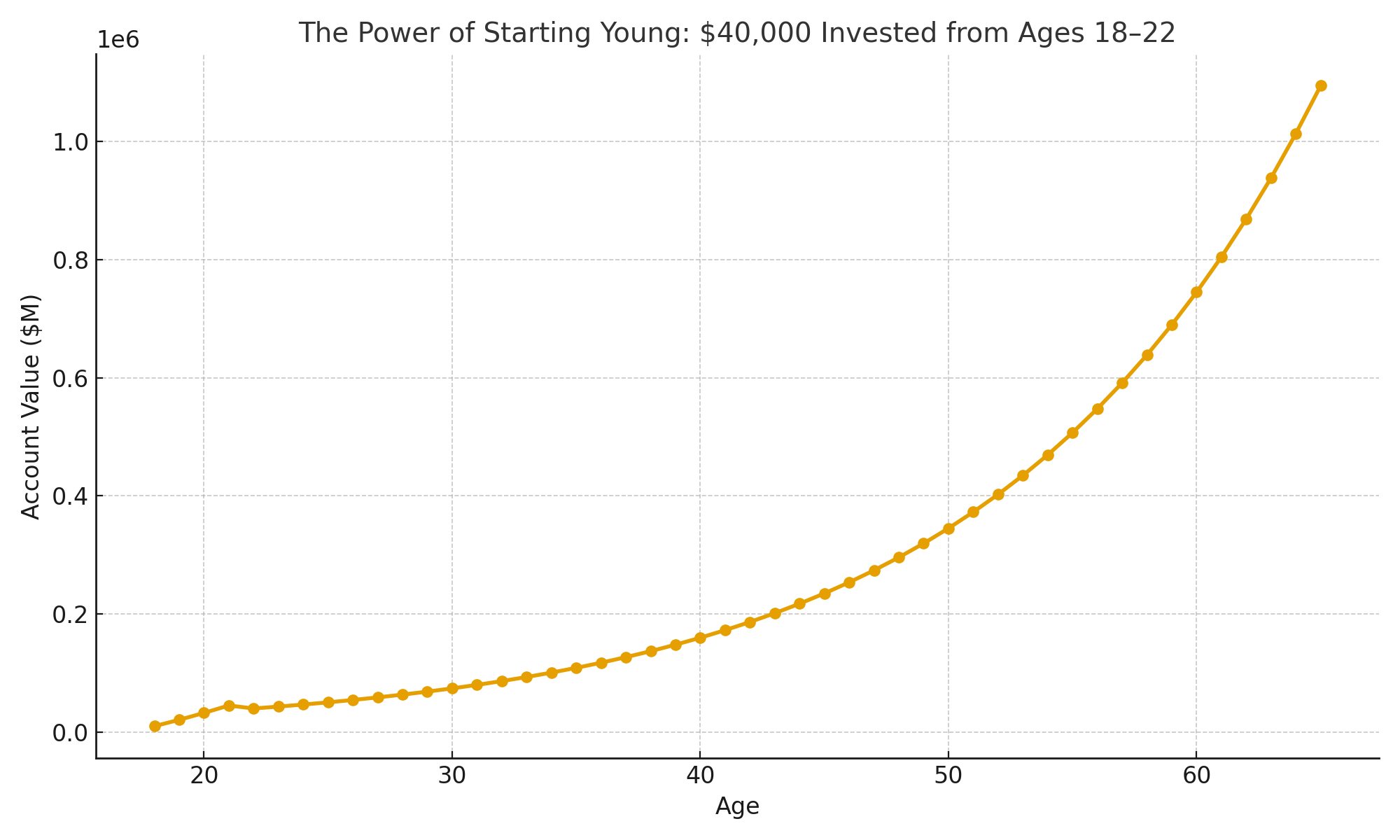

Let’s illustrate the power of starting young. Say an athlete contributes $10,000 each year for four years (ages 18–22) to an investment account – a total of $40,000 invested. If they never add another penny afterward, and the money grows at an average 8% yearly return, by age 65 that account could be worth over $1.2 million! That’s the magic of about 40 years of compounding. Even much smaller amounts make a big difference when you have decades ahead.

Key advice: once you invest money for the long term, try not to touch it. Let it grow. It might be tempting down the road to dip into your investment account for a fancy purchase, but every time you withdraw, you break the compounding snowball. Give your retirement savings 40+ years to compound and grow – you’ll be glad you did. Think of it like a seed you plant now; if you keep digging it up, it won’t turn into a strong tree.

One of the best ways for a young person to invest for the future is a Roth IRA, which we’ll cover next. But even beyond retirement accounts, if you’ve maxed those out, you can invest in regular brokerage accounts. The priority is to get your money growing. It may feel slow at first – investing is not a get-rich-quick scheme – but as the years pass, you’ll see that little by little, your money is making money, and that’s how wealth is built.

Note: Axon Capital Management does not guarantee a 8% return; this rate was used solely for illustrative purposes to demonstrate the potential long-term impact of early investing.

A Roth IRA (Individual Retirement Account) is essentially a special investment account for retirement. What makes it special? Contributions to a Roth IRA are made with after-tax dollars (money you’ve already paid taxes on), and then all the growth and future qualified withdrawals are tax-free. In other words, you pay taxes on your NIL earnings now, put some of that money into a Roth IRA, and when you take it out in retirement, you owe no taxes on the gains. If your investments double, triple, or grow many times over across 40+ years, all that growth is yours to keep, tax-free.

The beauty of a Roth IRA is in the long-term payoff. You might not fully appreciate it at 20, but having a pot of money growing tax-free for retirement is like giving a gift to your 60-year-old self. To reinforce how powerful this can be: imagine by the time you’re 23 you’ve contributed, say, $20,000 total into a Roth IRA. If that grows at an average rate and ends up being $200,000 or $300,000 by retirement (which is very possible over decades), none of the increase will be lost to taxes. That could mean tens of thousands of extra dollars for you, just by choosing the Roth vehicle.

Beyond Roth IRAs, if your NIL earnings are very high, you have other retirement savings options too. Because many athletes under NIL are considered independent contractors, you might be eligible to open a Solo 401(k) or an SEP-IRA (Simplified Employee Pension IRA) as a “business owner” of your own brand. These accounts have much higher contribution limits, allowing you to shelter more of your income for retirement and even get some current-year tax breaks. This is a bit more advanced, and an Axon financial advisor can help set it up correctly.

In summary: take advantage of tax-advantaged retirement accounts while you can. Max out a Roth IRA for tax-free growth. If you’re earning way more than the Roth limit, consider other self-employed retirement plans to stash money away. These moves will not only save you on taxes but also instill a habit of investing for the long haul.

NIL earnings aren't gifts—they're taxable income classified as self-employment because you're running your own personal brand business. That means you owe federal income tax, state income tax (in most states), and self-employment tax for Social Security and Medicare. Unlike a W-2 job where taxes are automatically withheld, NIL income arrives in full and it's your responsibility to handle the tax bill. Many athletes are blindsided when a $100,000 NIL deal nets closer to $60,000 after taxes.

NIL deals typically pay via 1099 forms with zero tax withholding. If you'll owe $1,000+ in taxes for the year, the IRS requires quarterly estimated payments—due in April, June, September, and January. Missing deadlines triggers penalties and interest even if you eventually pay. Work with a CPA to calculate safe harbor payments (typically 100-110% of last year's tax or 90% of current year estimates) to avoid surprises.

Consider setting aside 30-40% of every NIL payment immediately. Federal income tax ranges from 10-37%, self-employment tax adds 15.3%, and state taxes vary from 0-13%. High earners in states like California face combined rates exceeding 50%. Open a separate savings account exclusively for taxes and treat it as untouchable—if you receive $50,000, move $15,000-$20,000 to tax savings immediately.

The biggest mistake: spending NIL money without reserving for taxes, then facing bills you can't pay. Second is failing to track deductible expenses—agent fees, travel, equipment, and training costs offset taxable income but only if documented. Third is ignoring multi-state tax obligations when deals cross state lines. Finally, many don't realize NIL income affects financial aid and scholarship eligibility—what looks like free money can reduce your aid package dollar-for-dollar. Work with a tax professional before signing deals, not after receiving a tax notice.

A fiduciary is legally obligated to act in your best interest at all times—no exceptions. Fee-only means they're paid exclusively by you through transparent fees or a percentage of assets managed, never through commissions for selling products. This combination eliminates the conflict of interest that plagues many "advisors" who push investments or insurance to earn kickbacks. When your advisor only profits if your wealth grows, your goals align perfectly—they have zero incentive to steer you toward deals that benefit them at your expense.

Inexperienced, wealthy young athletes are prime targets for quick commissions and scams. The NIL landscape is still the Wild West, with operators pitching sketchy investments, overpriced insurance products, and bad endorsement deals buried in fine print. Many people see a 19-year-old with sudden six-figure income and assume they're an easy mark. Without professional protection, athletes get pressured by friends, family connections, and strangers into "opportunities" that drain wealth fast. The vulnerability isn't just financial inexperience—it's also the spotlight, the pressure to say yes, and the fear of missing out on the next big thing.

A good fiduciary advisor educates you on budgeting, credit management, compound interest, and the time value of money while helping set up investment accounts, retirement plans, and proper insurance. They create tax strategies to minimize your hit, ensure you're setting aside enough quarterly, and review every opportunity that comes your way—filtering out bad deals before you sign. Most importantly, they force you to think beyond college, preparing you for life after sports whether that's a pro career, another profession, or ensuring your money lasts if you never see another big paycheck. Include family in the process too—parents provide grounding, a second set of eyes, and voice of reason on big decisions.

In conclusion, NIL money can be a blessing or a curse – the outcome depends on how you handle it. By following general financial principles like budgeting, saving, and investing, understanding and managing your tax obligations, and using smart strategies like Roth IRAs, trusts, and good advisors, you can turn a few golden years of earnings into a lifetime of security. This is a pivotal moment: you have a chance to avoid the fate of those athletes who earn a fortune and end up with nothing. Instead, you can be the example of an athlete who used their Name, Image, and Likeness not just to make money, but to build wealth that lasts.

Stay humble, stay hungry (both in sports and financial learning), and know that every wise choice you make now is a step toward a stable and successful future off the field. Your future self – and your family – will be glad you played this money game wisely and for the long run.

If you have any questions or would like to speak with a financial advisor, please contact us by filling out the form below.

Article written by Brady Lochte, founder of Axon Capital Management and a fee-only fiduciary financial advisor serving individuals and families across the Austin metro area. Brady is committed to providing clear, transparent financial guidance that helps people navigate retirement, investing, and long-term planning with confidence.

Disclaimer: This article is for informational and educational purposes only and does not constitute investment, legal, or tax advice. Axon Capital Management is a registered investment advisor. Readers should consult with their own financial, legal, and tax professionals before making any decisions based on the content of this article. Past performance is not indicative of future results. All examples and strategies discussed are illustrative and may not be suitable for all individuals.

Please submit the form with any questions or comments and I'll be in touch shortly.

If you'd rather not wait, you can also book a time directly on my calendar using the link below:

Schedule a call