When searching for a financial advisor in Texas, you'll find thousands of options. But if you're specifically looking for a fee-only fiduciary advisor, your choices narrow dramatically. In fact, it’s estimated that fewer than 2% of financial professionals nationwide operate on a truly fee-only basis. In a state as large as Texas, this translates to only a few hundred fee-only advisors serving millions of households.

Even within Texas, fee-only advisors tend to cluster in major metros like Austin, Dallas, Houston, and San Antonio, where investor demand, higher incomes, and more sophisticated planning needs make a client-paid advisory model more viable. Outside of these areas, truly fee-only options become much harder to find.

At Axon Capital Management, we're proud to be part of the Texas fee-only community. But the rarity of fee-only advisors raises an important question: why are there so few, and why should it matter to you?

The financial advisory industry is filled with confusing terminology, and the distinction between fee-only, fee-based, and commission-based advisors is one of the most important - and most misunderstood.

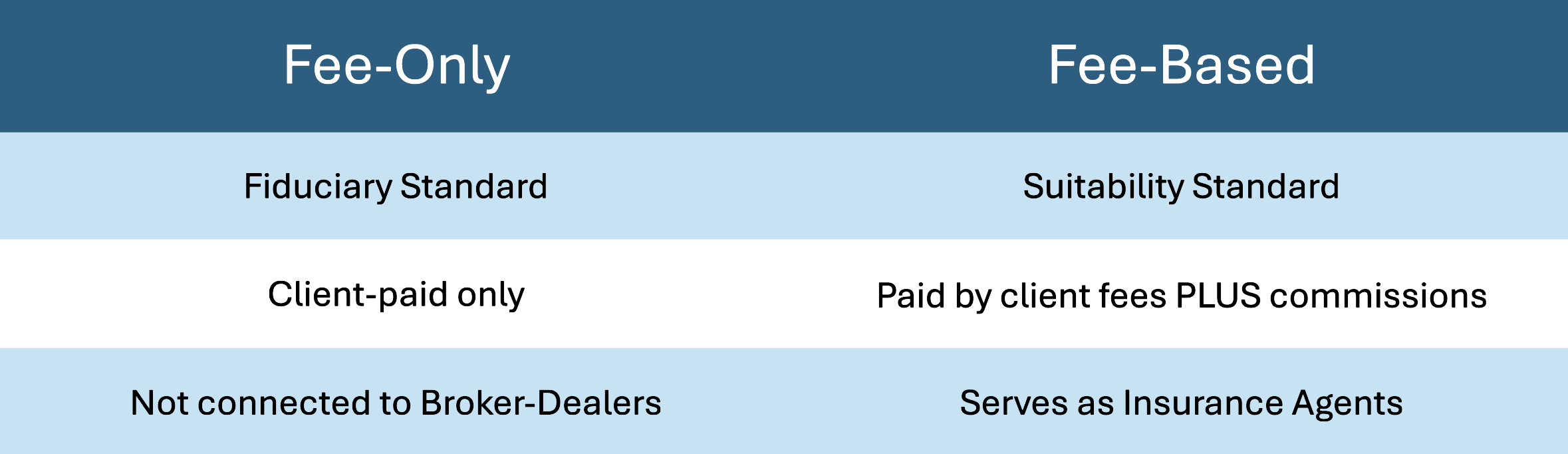

Fee-only advisors are compensated exclusively by their clients. They don't receive commissions from selling financial products, nor do they accept referral fees or any other third-party compensation. Their only source of income is the fees you pay them directly, typically as a percentage of assets under management, an hourly rate, or a flat fee.

Fee-based advisors can charge fees AND receive commissions. Despite the similar-sounding name, this is fundamentally different. These advisors might charge you a planning fee while also earning commissions when you purchase certain investments or insurance products they recommend.

Commission-based advisors earn money primarily through commissions on the products they sell—mutual funds, insurance policies, annuities, and other financial products.

The difference isn't just semantic. It's about incentives, conflicts of interest, and who the advisor is truly working for.

If fee-only advice eliminates conflicts of interest and aligns the advisor's interests with the client, why do fewer than 2% of advisors operate this way?

The traditional financial services model is built on product sales. Insurance companies, mutual fund companies, and brokerage firms train and support advisors to sell their products in exchange for commissions. This infrastructure has existed for decades and makes it relatively easy for someone to enter the industry and start earning income quickly.

Speaking from personal experience, building a fee-only practice requires a lot of entrepreneurial effort. You're not supported by a large product manufacturer. You have to build your own business, create your own systems, and attract clients based on the value of your advice rather than the appeal of a particular product.

Commission-based advisors can earn substantial income from a single product sale. A fee-only advisor building long-term client relationships may earn less initially but builds more sustainable, recurring revenue over time. Many aspiring advisors need immediate income and can't afford the slower build that fee-only models often require.

Fee-only advisors typically register as Registered Investment Advisors (RIAs) with the SEC or state regulators, which comes with stricter fiduciary obligations and compliance requirements. While these regulations protect consumers, they also create barriers to entry that discourage some advisors.

Many clients don't understand the difference between fee-only and other compensation models. If consumers don't know to ask for fee-only advice, there's less market demand driving advisors to adopt this model.

Here's why the fee-only distinction matters so much: compensation drives behavior.

Imagine you're deciding whether to invest in a low-cost index fund or a more expensive actively managed fund. If your advisor earns a higher commission selling the actively managed fund, which one do you think they're incentivized to recommend?

Or consider insurance products. Whole life insurance policies can generate substantial commissions, sometimes 50-100% of the first year's premium. Term life insurance, which is often more appropriate for many families, generates far smaller commissions. A commission-based advisor has a financial incentive to recommend whole life, even when term insurance better serves your needs.

These conflicts aren't always nefarious. Many advisors genuinely believe they're recommending suitable products. But the conflict exists whether or not the advisor is conscious of it. Behavioral psychology has shown that financial incentives influence our decisions, even when we think we're being objective.

Fee-only advisors operate under a fiduciary standard, meaning they're legally required to act in your best interest at all times. This is the highest standard of care in the financial industry.

Many other advisors operate under a suitability standard, which only requires that recommendations be "suitable" for the client—not necessarily the best option available. A product can be suitable while still being more expensive, less tax-efficient, or otherwise inferior to alternatives that would serve you better.

The difference between "best interest" and "suitable" might seem subtle, but it can cost you tens or hundreds of thousands of dollars over a lifetime of investing.

There’s no single public database that clearly labels advisors as fee-only, since regulators track registration status rather than compensation models. Still, industry data offers useful context: nationwide, only about 15–20% of CFP® professionals identify as fee-only, and Texas—despite having tens of thousands of licensed financial advisors—has only a small minority operating under a strict fee-only model. Those advisors are heavily concentrated in major metros like Austin, Dallas, Houston, and San Antonio, with far fewer options in suburban or rural areas.

For a Texas investor searching “financial advisor near me,” this matters. The odds strongly favor landing on a commission or fee-based advisor unless you know exactly what to look for and how advisors are actually compensated.

This scarcity creates challenges for investors seeking conflict-free advice:

Finding a fee-only advisor takes more effort. You can't just walk into any branch of a major financial services firm and expect to work with a fee-only advisor. You have to specifically search for one.

Not all "fiduciary" claims are equal. Some advisors claim to act as fiduciaries while still accepting commissions. True fee-only advisors are fiduciaries 100% of the time because their compensation structure doesn't allow for anything else.

Fee transparency varies. Fee-only advisors clearly disclose what you're paying. With commission-based products, the fees are often embedded in the product itself, making it harder to understand exactly what you're paying and whether it's reasonable.

The concentration of fee-only advisors in major metros creates a particular challenge for rural Texans. If you live in Lubbock, Amarillo, Tyler, or smaller communities across the state, you likely don't have a fee-only advisor within driving distance.

Axon Capital Management serves clients throughout Texas through a virtual advisory model. Secure video conferencing, digital document sharing, and online portfolio access mean you receive the same comprehensive fee-only planning whether you're in Austin or a small town three hours away. For Texans who don’t have a fee-only option down the road, virtual planning bridges the gap.

If you're searching for a fee-only advisor in Texas, here's how to verify their compensation model:

1. Check their Form ADV Part 2

All RIAs must file this document with regulators, and it discloses their compensation structure. If it mentions commissions, referral fees, or third-party compensation, they're not fee-only.

2. Ask directly

Simply ask: "Are you fee-only, meaning you receive no commissions or compensation from anyone other than your clients?" Listen carefully to the answer. If it's not a clear "yes," dig deeper.

3. Understand their business model

Ask how they're compensated. Fee-only advisors typically charge:

I chose the fee-only model at Axon Capital Management because I believe it's the only way to truly serve Texas. We don't accept commissions, we don't receive referral fees, and we don't have hidden revenue streams.

Our compensation is simple and transparent: you pay us directly for our advice and wealth management services. Our success is tied to your success, not to how many products we can sell.

This structure allows us to focus on what matters most: integrated wealth planning that addresses your unique goals, challenges, and opportunities. Whether you're navigating stock compensation from a tech company, planning for retirement, or simply trying to make smarter financial decisions, our advice is driven by one question: what's best for you?

In a state with thousands of financial advisors, fewer than a few hundred operate on a truly fee-only basis. This rarity isn't because the fee-only model doesn't work—it's because it requires advisors to build sustainable businesses based on the value of their advice rather than product commissions.

For you as an investor, this scarcity means you need to be intentional about finding a fee-only advisor if conflict-free advice matters to you. The good news is that once you find one, you'll be working with an advisor whose financial success is directly tied to yours—no hidden agendas, no product quotas, just advice designed to help you achieve your financial goals.

Axon Capital Management is proud to serve clients across Texas with fee-only financial advice. If you're looking for financial guidance from an advisor who works exclusively for you, please reach out by filling out the contact form below.

Article written by Brady Lochte, founder of Axon Capital Management and a fee-only fiduciary financial advisor serving individuals and families across the Austin metro area. Brady is committed to providing clear, transparent financial guidance that helps people navigate retirement, investing, and long-term planning with confidence.

This article is for educational purposes only and should not be considered personalized financial advice. The information about fee-only advisors is based on industry research and publicly available data. Individual circumstances vary, and you should consult with a qualified financial professional about your specific situation.

Please submit the form with any questions or comments and I'll be in touch shortly.

If you'd rather not wait, you can also book a time directly on my calendar using the link below:

Schedule a call